TL;DR

- The Board of Peace is discussing a potential stablecoin for Gaza as part of reconstruction planning, but the structure behind that proposal remains undefined.

- A dollar-pegged token requires reserves, redemption rails, compliance controls, electricity, and telecom stability. Code alone does not create a payment system.

- Without reliable power, communications resilience, banking access, and regulatory clarity, large-scale rollout would be premature.

U.S. President Donald Trump’s newly launched Board of Peace is discussing whether a U.S. dollar‑pegged stablecoin could be used in the Gaza Strip as part of reconstruction efforts.

The Gaza stablecoin proposal has surfaced in media reports citing people familiar with the discussions. The board did not release any formal policy document, and neither has it issued a detailed framework explaining how such a system would operate.

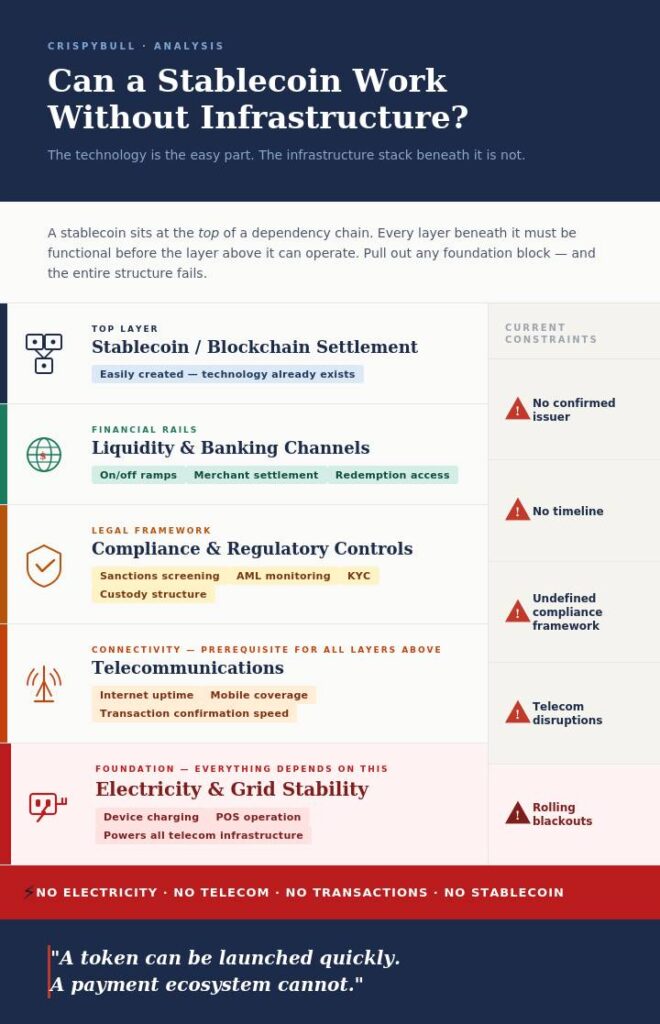

Most coverage has focused on political implications. However, the more immediate question is operational: Can a fully digital payments system function reliably under current conditions in Gaza?

Stablecoins rely on electricity, telecommunications, access to banking services, liquidity conversion, and regulatory oversight. Without those foundations, the technology alone does not create a functioning payment system.

Who Is Involved in the Discussions?

Reporting has consistently identified technology entrepreneur Liran Tancman as a participant in the discussions. He is described as advising on the technical feasibility of a dollar‑pegged token within the broader reconstruction framework.

The Board of Peace formally launched in January 2026 with President Trump as its Chair. The board’s reported executive and Gaza‑focused committees include figures such as Jared Kushner, Marco Rubio, Steve Witkoff, Tony Blair, and Nikolay Mladenov.

There has been no official announcement confirming a rollout structure. At this stage, the Gaza stablecoin proposal remains exploratory.

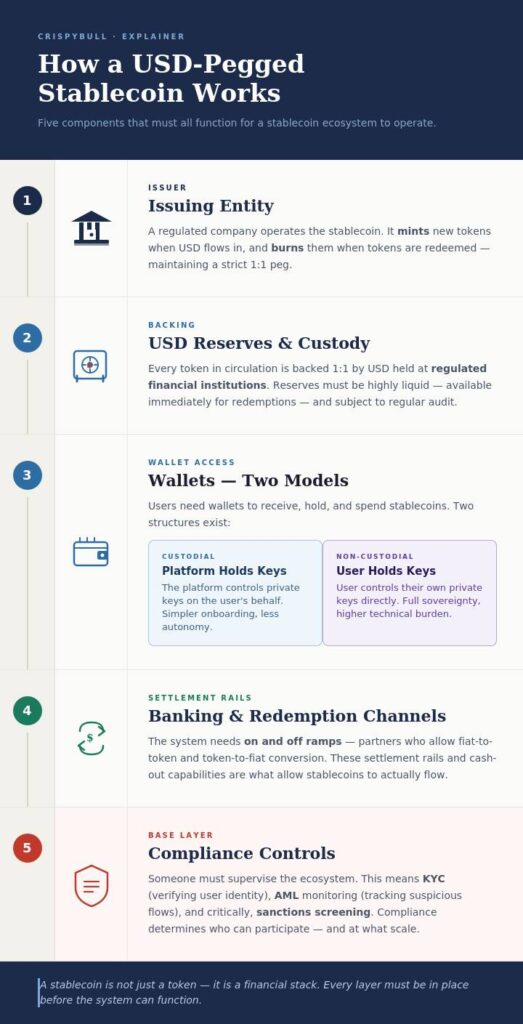

How Stablecoins Normally Operate

In practice, a U.S. dollar‑pegged stablecoin is not just software. It is a financial structure built around reserves, banking access, and compliance.

An issuing company creates tokens against dollar reserves. Those reserves sit in regulated financial institutions and are subject to oversight. Without verified reserves, the peg does not hold.

Users access the token through wallets. In a custodial model, a platform controls private keys and manages compliance. In a non‑custodial model, users hold their own keys and assume that responsibility themselves.

Crucially, the token must be redeemable. Banking partners convert tokens back into fiat currency. If redemption channels fail or narrow, confidence erodes, and parity breaks down.

Compliance is not peripheral. Sanctions screening, anti‑money laundering controls, transaction monitoring, and customer identification determine whether financial institutions can participate at all.

Issuance is the visible layer. Redemption, settlement certainty, and regulatory acceptance are what make a stablecoin function as money rather than as a tradable digital asset.

So far, the proposal has not publicly identified an issuing authority, reserve custodian, governing jurisdiction, or banking partner for the system it envisions.

Gaza’s Monetary Environment

Gaza does not issue its own currency. The Israeli New Shekel remains the primary legal tender, and the U.S. dollar is also widely used in commercial activity.

The Palestinian Monetary Authority conducts banking oversight. However, the banking system depends on cross‑border clearing arrangements and has experienced periodic cash shortages during border restrictions.

Any digital dollar layer would therefore enter an existing multi‑currency environment rather than replace it. External clearing access and physical cash constraints are already shaping liquidity flows.

Electricity and Payment Reliability

Digital payments require consistent access to charged devices and functioning networks.

Gaza experiences rolling blackouts due to damaged infrastructure, affecting grid stability. When electricity is unavailable, users cannot access digital wallets, even if balances are recorded on a blockchain.

Retail commerce depends on predictability. If payment access becomes intermittent, merchants may hesitate to rely on it. In environments where electricity supply is unreliable, physical cash typically reasserts itself as the primary medium of exchange.

The Gaza stablecoin proposal assumes sufficient power stability to support daily transactions. Yet no public timeline has been presented for restoring durable grid reliability, raising sequencing concerns about deploying an electronic settlement layer before core infrastructure resilience has been reestablished.

Telecommunications and Transaction Confirmation

Stablecoin transactions require internet connectivity for broadcasting and confirmation.

Telecom disruptions can delay confirmation windows and increase settlement uncertainty. Merchants may be reluctant to accept payments that cannot be confirmed within predictable timeframes.

Even custodial wallet systems depend on backend servers that must remain online. Connectivity, therefore, affects both decentralized and centralized models. As with electricity, policymakers have not presented a clear public timeline for restoring telecom resilience at scale, which reinforces concerns about introducing a digital settlement system before communications stability is in place.

Compliance and Sanctions Considerations

Hamas still governs Gaza and remains a designated terrorist organization by several jurisdictions.

Any U.S. dollar‑pegged instrument operating in Gaza would require robust sanctions screening and transaction monitoring systems. Financial institutions participating in a potential rollout would face compliance obligations under U.S. law.

Issuers would need defined customer identification standards, wallet verification procedures, transaction monitoring systems, and redemption controls. No public compliance framework has been released.

Liquidity and Conversion Mechanics

A digital token must integrate with the real economy.

Users would need reliable mechanisms to convert shekels into tokens and tokens back into usable funds. Merchants would require clarity on settlement currency, exchange rate handling, and access to working capital.

Without stable banking partners and predictable redemption channels, liquidity conversion becomes the primary bottleneck.

These operational mechanics are central to evaluating the Gaza stablecoin proposal.

Timeline and Sequencing

This Gaza stablecoin plan remains an informal proposal with no publicly confirmed launch timeline. As outlined in the previous sections, multiple technical, regulatory, and infrastructure prerequisites would need to be addressed before a rollout could become operationally feasible.

Reconstruction governance under the Board of Peace is still evolving. Energy, telecom, and banking systems remain under strain. While issuing a token is technically straightforward, building a resilient payment ecosystem requires coordinated regulatory approval, financial partnerships, infrastructure stabilization, and merchant integration.

Policymakers must therefore evaluate the Gaza stablecoin proposal within the broader reconstruction sequence rather than treat it as a standalone technology initiative.

Conclusion

The Gaza stablecoin proposal is being discussed as a reconstruction tool. On paper, a digital dollar layer promises efficiency, transparency, and faster payments. In practice, it would sit on top of systems that are still unstable. Power supply remains inconsistent. Telecom resilience has not been publicly benchmarked. Banking channels and compliance architecture are not yet defined.

A blockchain token can be launched quickly. A functioning payments ecosystem cannot.

Before an electronic settlement layer can operate at scale, electricity, connectivity, liquidity conversion, and regulatory clarity must be demonstrably in place. Until then, the Gaza stablecoin proposal remains a concept under discussion rather than an executable payments system.