TL;DR

- CoinDesk’s April 2026 report data shows the stablecoin sector continuing to expand despite relatively muted conditions across broader crypto markets.

- Tether strengthened its market leadership while synthetic stablecoin models faced renewed pressure following DeFi-related stress events.

- Tokenized Treasuries and tokenized equities continued attracting institutional adoption, signaling deeper integration between blockchain infrastructure and traditional finance.

The latest CoinDesk stablecoin market report may look, at first glance, like another routine month of rising market caps and expanding tokenized assets. But the April 2026 data reveals something more important happening beneath the surface.

Crypto’s center of gravity is shifting.

The strongest growth in the industry is no longer coming from speculative DeFi experiments or retail trading mania. Instead, capital is increasingly flowing into products designed to resemble traditional financial infrastructure: tokenized Treasuries, yield-bearing money market funds, institutional collateral systems, and stablecoins deeply integrated into payment and settlement rails.

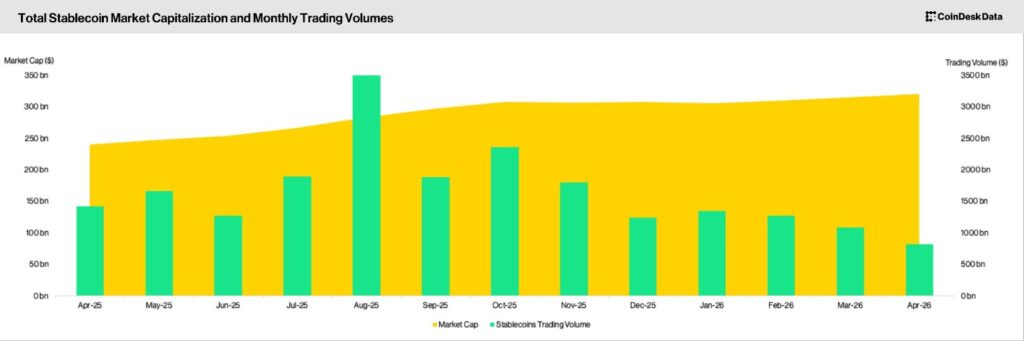

According to CoinDesk’s April 2026 figures, the total stablecoin market cap climbed to a record $321 billion, while tokenized real-world assets reached $26.7 billion. At the same time, some of the market’s more complex synthetic structures continued to unwind under pressure. The contrast may be one of the clearest signs yet that the digital asset sector is entering a more mature and institutional phase.

The Market Rewarded Stability, Not Complexity

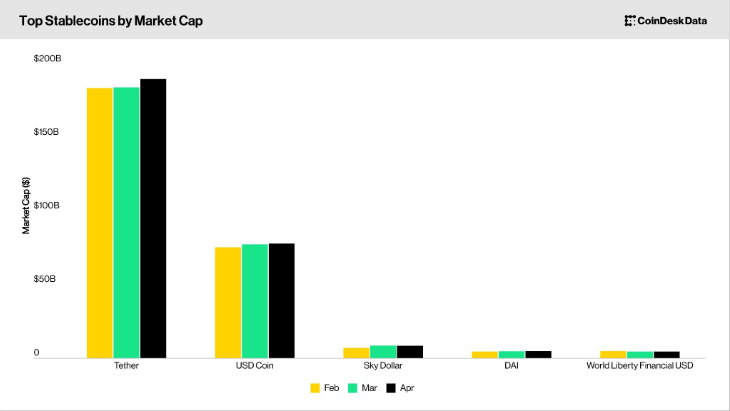

One of the most revealing developments in the report was the widening gap between Tether’s performance and the continued decline of Ethena’s USDe.

USDT expanded its market cap to $190 billion in April, accounting for most of the growth in the broader stablecoin market during the month. Its market share rose back to 59.2%, while its dominance in centralized exchange trading volumes remained overwhelming at 73.6%.

That growth did not happen in isolation.

Tether increasingly behaved less like a stablecoin issuer and more like a liquidity provider for the broader market. Following Drift Protocol’s $285 million exploit, Tether committed up to $127.5 million to support recovery efforts. Drift later switched its settlement infrastructure from USDC to USDT, effectively strengthening Tether’s position inside Solana-based trading activity.

At the same time, USDe experienced the opposite trajectory.

Ethena’s synthetic dollar lost 36.1% of its market capitalization during April, falling to its lowest level since October 2024. The decline followed the broader fallout from the KelpDAO exploit, which exposed vulnerabilities tied to leveraged DeFi positions and recursive borrowing strategies.

The market reaction was telling.

Investors appeared increasingly uncomfortable with stablecoin structures dependent on perpetual futures exposure and complex yield engineering. Ethena itself responded by drastically reducing its perpetual futures exposure and shifting reserves toward overcollateralized institutional lending and traditional fixed-income instruments.

In practice, one of crypto’s most aggressive synthetic stablecoin projects moved closer to traditional finance after market stress exposed the fragility of its earlier model.

>>> Read more: How Tether Commodity Lending Is Reshaping Trade Finance

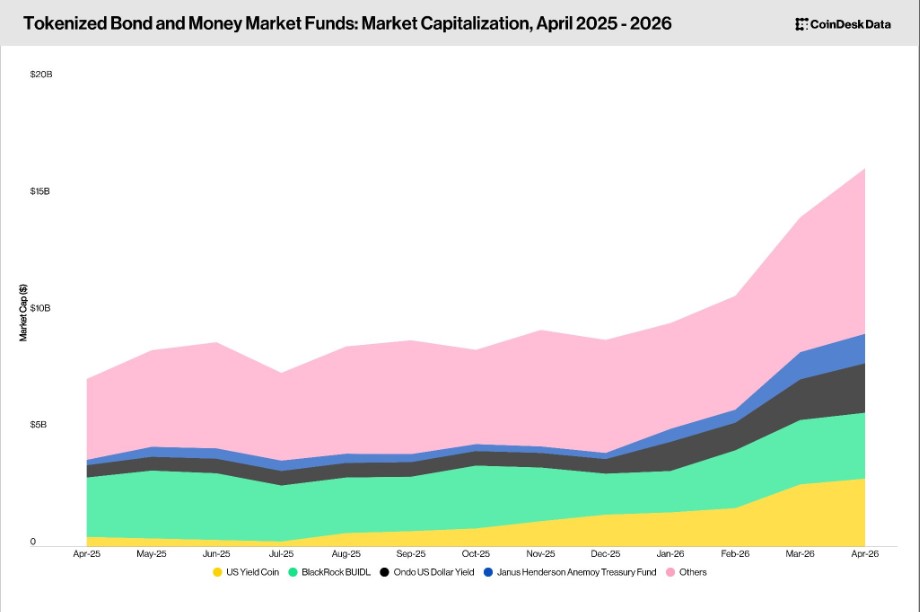

Tokenized Treasuries Are Becoming Crypto’s Institutional Core

While speculative DeFi structures struggled, tokenized Treasuries continued to expand rapidly.

CoinDesk’s report showed tokenized bond and money market fund products growing to $16.2 billion in market capitalization during April. The sector now represents more than 60% of the entire tokenized asset market.

This matters because tokenized Treasuries solve a real institutional problem.

Large pools of capital want blockchain-based settlement efficiency without abandoning regulated yield-generating products. Tokenized money market funds allow institutions to hold Treasury-backed assets on-chain while preserving liquidity and collateral flexibility.

That explains why products like Circle’s USYC and BlackRock’s BUIDL are growing aggressively.

USYC overtook BUIDL in April to become the largest tokenized fund product, while BlackRock continued expanding BUIDL’s integration into institutional trading infrastructure. On April 28th, OKX enabled BUIDL as yield-bearing collateral through a partnership involving Standard Chartered.

This is no longer a niche crypto experiment. Traditional financial instruments are gradually becoming interoperable with blockchain-based trading systems.

Tokenized Real-World Assets Are Gaining Momentum Beyond DeFi

Another underappreciated trend in the report was the acceleration of tokenized equities.

The sector expanded 22% during April to reach a record $1.59 billion. While that figure remains small compared to stablecoins, the speed of growth is notable because tokenized equities increasingly move the conversation beyond crypto-native trading.

The key development was not simply higher market capitalization.

Ondo Finance announced a partnership with Broadridge Financial Solutions allowing holders of more than 250 tokenized stocks and ETFs to review company filings and submit shareholder voting preferences directly through crypto wallets.

That may sound procedural, but it represents something larger. The industry is slowly rebuilding pieces of traditional capital markets infrastructure on-chain. For years, tokenization narratives focused mainly on fractional ownership and 24/7 trading. The newer focus is operational integration: governance, collateral mobility, settlement efficiency, and institutional accessibility.

That transition is significantly more important for long-term adoption.

Stablecoins Are Becoming Financial Infrastructure

Perhaps the most important conclusion from CoinDesk’s April market report is that stablecoins are no longer behaving primarily as crypto trading tools.

Major developments during the month included:

- Meta launching USDC creator payouts through Stripe

- Robinhood expanding access to USDG

- Morgan Stanley introducing a stablecoin reserve portfolio

- Banking Circle launching stablecoin settlement services

These are infrastructure developments.

The companies involved are not positioning stablecoins as speculative assets. They are positioning them as payment rails, settlement layers, collateral systems, and treasury-management tools.

That distinction matters because infrastructure markets tend to consolidate around scale, liquidity, regulatory clarity, and trust.

April’s data suggests that consolidation is already happening.

>>> Read more: Tether-Backed Rumble Brings Bitcoin Tipping to Creators

The Industry Is Starting to Look More Like Finance

The April stablecoin market report ultimately revealed a crypto industry moving closer to traditional financial architecture rather than further away from it.

The strongest growth came from:

- tokenized Treasuries,

- institutional collateral products,

- regulated yield-bearing assets,

- and dominant liquidity providers.

Meanwhile, some of the market’s most complex DeFi structures faced renewed pressure under real-world stress.

Speculative innovation is not disappearing from crypto markets. But April’s data suggests the industry is entering a different stage of growth, where adoption and integration are accelerating faster than purely experimental narratives.

The strongest momentum is now concentrated around products and infrastructure that connect blockchain systems with real financial activity: payments, settlement, collateral management, Treasury products, and tokenized capital markets.

Rather than slowing down, the industry increasingly appears to be moving deeper into the global financial system.