TL;DR

- Kraken issued more than 56 million crypto tax forms tied to 2025 transactions under new U.S. reporting rules.

- A large share of reported activity involves low-value transactions, raising questions about reporting efficiency.

- The rollout highlights growing compliance pressure and fuels calls to refine crypto tax rules.

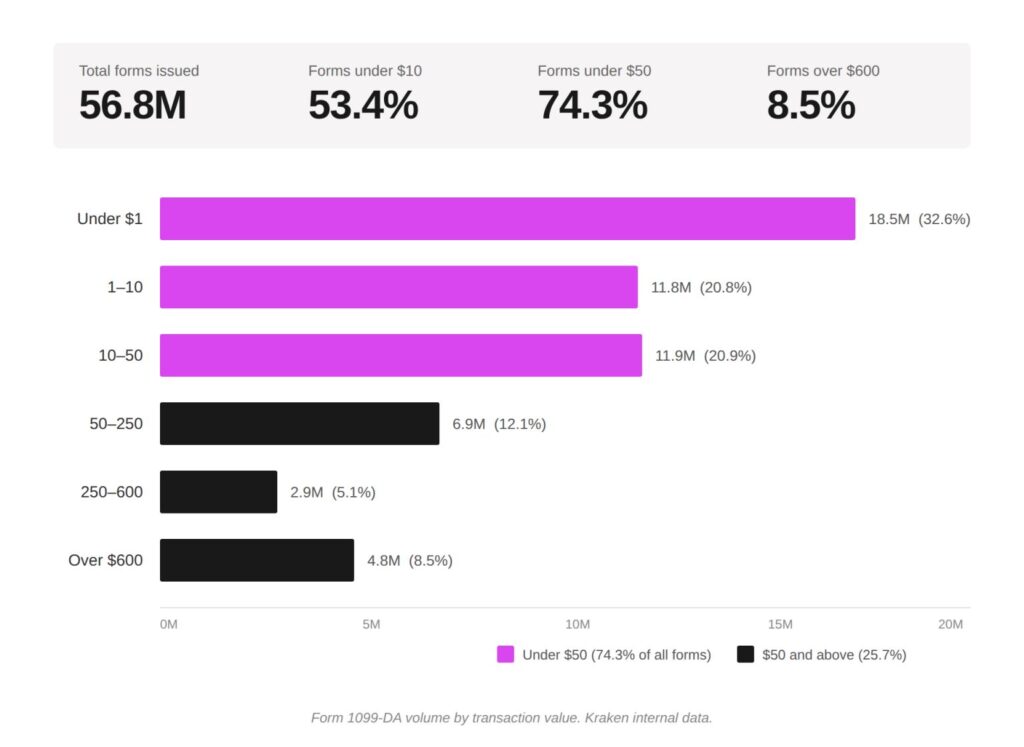

Kraken says it submitted more than 56 million Form 1099-DA filings tied to customers’ 2025 activity, giving the market one of the clearest early looks at how the new U.S. digital asset reporting rules are working in practice. The scale is the headline, but the deeper story is what the filings reveal about the burden the new U.S. digital asset tax reporting rules load onto both exchanges and everyday users.

The exchange said nearly a third of the forms, or about 18.5 million, covered transactions worth less than $1. More than half were for $10 or less, and nearly three-quarters were for under $50. Kraken argues that many of these records relate to routine account activity, small purchases, and tiny staking rewards rather than large speculative trades.

A first real test of Form 1099-DA

The IRS finalized digital asset broker reporting rules in 2024, with gross proceeds reporting starting for transactions effected on or after January 1, 2025. IRS instructions for Form 1099-DA say brokers are not required to report basis information for 2025 transactions, with broader basis reporting generally beginning in 2026.

That makes the 2025 tax year a transition period. Users may receive forms showing proceeds without the full cost-basis context needed to calculate taxable gains or losses. This can create confusion for people who hold assets across multiple exchanges and wallets. Kraken said that disconnect drove thousands of customer questions during the filing season.

>>> Related: IRS Cryptocurrency Tax Reporting 2025: What You Need to Know

Why the Kraken’s crypto tax reports matter

The filing volume matters because it shows how crypto reporting differs from many traditional financial tax workflows. According to Kraken’s own figures, only 8.5% of the forms exceeded $600. That threshold commonly applies to reporting in other parts of the tax code but does not apply to crypto transactions. Therefore, a huge number of very small transactions flow into a system that was not built with micro-rewards and high-frequency blockchain activity in mind.

For readers outside crypto, the significance is practical. A person may now receive tax reporting connected to very small digital asset disposals or staking-related activity, even when the dollar amount appears trivial. While the tax owed may not be large, but the record-keeping burden can grow quickly.

Paper delivery adds to the reporting burden

Beyond filing with the IRS, exchanges are also required to provide copies of tax forms directly to users. Under long-standing rules for information returns, this has typically meant paper delivery by default unless a user explicitly consents to electronic tax form delivery.

At the scale seen in Kraken’s tax reporting, that requirement creates a significant operational layer. Platforms that operate entirely online would distribute tens of millions of physical documents, introducing printing costs, mailing logistics, and delays.

Recent proposals from the IRS aim to address this issue by allowing exchanges to default to electronic tax form delivery. The shift would not change reporting obligations, but it would reduce the need for large-scale paper distribution. Such rules would align the system more closely with how digital platforms operate.

Kraken turns compliance into a policy argument

Kraken is using the disclosure to push for two policy changes. First, it wants a meaningful de minimis exemption that would remove small, routine digital asset payments from capital gains reporting. Second, it wants Congress to let taxpayers choose whether staking rewards tax treatment applies when rewards are received or when they are sold, rather than forcing tax treatment at the moment of receipt.

The exchange argues that current treatment can create a mismatch between taxable income and real economic gain, especially when staking rewards are worth only fractions of a cent at the transaction level. That position is likely to resonate with industry groups. Lawmakers, however, would still need to balance simplification against tax enforcement and revenue concerns.

>>> Read more: What is CARF 2027

What comes next

The first year under these new tax reporting rules was always likely to expose friction points. Kraken’s numbers now offer a concrete example of where those frictions sit. The immediate takeaway is that the current rules may capture a large volume of low-value activity, adding compliance work without clearly improving tax clarity for users.

The debate around crypto tax reporting is likely to move beyond one exchange’s filing count, though Kraken highlights the scale of the issue. As basis reporting expands, more platforms will work through the same requirements. Pressure on Washington might grow quickly to refine rules around micro-transactions and staking rewards.