We are sitting at Proof of Talk in Paris, a summit drawing an increasingly institutional crowd to the question of what decentralized finance and AI become at scale. The room outside is full of asset managers, sovereign wealth fund representatives, and policy people from three continents. And Marcus Graichen, known to virtually everyone in the Bittensor ecosystem simply as Mog, and the founder of Taostats, the network’s leading analytics platform, is explaining what it was like to update an HTML page every morning at nine o’clock.”

“We started as one man making an HTML site,” he says, without any particular sense that this is an unusual origin story for someone whose platform now processes the financial activity of one of the fastest-growing decentralized AI networks in the world. “I wasn’t seeking venture capital funding for that. It was just a hobby project.”

Mog is not what most institutional investors expect when they sit down with a leading infrastructure founder in this space. He knows it, and he seems to find it mildly amusing. “They always leave a little surprised,” he says. “I’m not sure I’m the standard persona that’s often put in front of these people.”

He is a multimedia graduate. He spent four years in Zanzibar running the digital operations of a professional kiteboarding company: websites, photography, marketing, coaching. He comes from two decades in web development and online publishing, not from machine learning or cryptography. And it turns out that background is precisely why Taostats exists, and why it works.

It Started With a Spreadsheet

Mog’s entry into Bittensor was through the front door that most serious participants use: he invested. In the early days of the network, there was a single subnet performing a task. Not particularly well, but well enough to demonstrate that the underlying architecture was sound. Returns were variable, so Mog kept spreadsheets, as he always had.

The problem was that getting the data to fill those spreadsheets required pulling it directly from the chain. It was technically demanding, and delivered nothing a normal person could read at a glance. The Discord channels weren’t much better.

“So initially, I just shared a spreadsheet with some extra columns of data that I thought related to actual funding and percentage APY and changes in that acquisition of funds,” he explains. “TaoStats formed in that sense that it was a shared visualization of the incentive layer of the network.”

That phrase “shared visualization of the incentive layer” is a precise description of something that the network was missing at the time. It had no public-facing interface. Participation required comfort with command lines and raw data outputs. Mog built the thing he personally needed, shared it, and watched other people need it too.

The Translation Problem

As the platform grew from spreadsheet to website, the second challenge came into focus: explaining what Bittensor was to people who had no machine learning background whatsoever. This is where Mog’s instinct for translation, honed across years of explaining digital businesses to clients and readers, found its purpose.

“It was early days of ChatGPT,” he says. “I used to say: when you ask ChatGPT a question, it’s like having one university professor in front of you, asking him a question and getting a response back, and that’s your response. What Bittensor was doing was filling a room full of a hundred professors and then asking that question to all of them, and then grading those answers, and then giving you back the best, however many you wanted, the top ten, the top fifty.”

It is, still, one of the clearest explanations of decentralized AI inference in plain language. “And people say: oh, I get that. That’s an amazing concept.”

Building Without a Cheque

The funding story of Taostats is unusual enough that it deserves to be told plainly, because it runs against almost every convention of how technology infrastructure gets built.

There was no seed round. There was no Series A. There was, for a period, a validator naming service. Mog spotted early that validators were about to compete for delegated stake, and that being identifiable would matter. He charged a modest fee, calibrated to what validators were earning, and when anyone questioned it, he had a ready answer drawn from his publishing background.

“I ran a female kitesurfing magazine online,” he says, “and there were women making startup bikini brands who will pay five thousand dollars for a month to get their product in front of a few hundred potential customers who might actually click through. You are looking at attracting thousands, if not tens of thousands, hundreds of thousands, millions of delegation. I’m asking for a very small amount.”

When staking went live, something unexpected happened. A couple of early miners who no longer wanted to run infrastructure joined as partners. Their collective stake pushed the Taostats validator into the top tier. And then, because Taostats was the thing everyone in the ecosystem visited every day, delegators started directing their stake there too.

“I actually felt guilt for this. I don’t deserve this. I shouldn’t have this.”

Instead of taking the runway and moving on, he went back to building. Subnets. API access. Education. Always managing the business carefully enough to survive a bear market. Always reinvesting rather than extracting. Jacob Steeves, the co-founder of Bittensor, kept telling him what to build next.

Turning Down DCG

This philosophy extended to equity conversations. There were approaches from people whose names would have looked impressive on a cap table. One of them was Barry Silbert of DCG.

“He said: we would like to support you. We don’t want to get involved. We love what you’re doing, but we’d like a stake in this.” Mog took the conversation seriously, went away and worked on the business structure that would make Taostats ready for that kind of partner. He came back, and turned it down.

“I can’t lie. All I would use your money for is to buy TAO. Which actually would have been a fantastic choice at the time. But I couldn’t do that. I’m not just taking your money to buy TAO. We don’t need it.”

His standing advice to founders in the ecosystem reflects what he lived: “Avoid equity until you really need it. Because the longer you hold onto your hundred percent, the more you have on the table to offer when it does come time. And also, take equity from those that are going to add value to your business.”

As of the day we speak in Paris, Taostats has still never taken on equity. “I feel like I know what I would need from a partner. We haven’t found that yet.”

What Institutional Investors Get Wrong

Grayscale has launched an ETF around Bittensor. Asset managers are arriving. The summit we are at exists precisely because these conversations are no longer hypothetical. So what does Mog see when they sit down across from him?

“It’s not a misreading,” he says carefully. “It’s a confusion. A confusion of allocation of capital.”

The confusion, specifically, is that institutional investors arrive asking for the VIP line, the preferential channel to acquire tokens. They assume the conversation is about token acquisition, when the actual question is more fundamental: are you investing in a business, a product, a founder, or a token? And are you bringing anything with you beyond capital?

“One of the most important things you can do as an investor is put money into something that you can add value to,” Mog says. “When people come to us and say, we’ve got an OTC, do you want to sell us OTC? And I say, well, what benefit is there for me to give you my tokens, either at a discount or at face value from my owner treasury, if you’re not adding something to it? For me, it’s a marketing cost. Are you helping me? Are you putting my name out there? Are you bringing in expertise and value?”

It is an inversion of the usual dynamic, the founder questioning the investor rather than the other way around. But it reflects something distinctive about how Bittensor’s ecosystem has developed: accountability runs in both directions.

The $30,000-a-Month Problem That Built a Business

Some of the most interesting companies get started because the founder couldn’t solve their own cost problem any other way.

Taostats was spending around $30,000 a month on RPC infrastructure, the technical layer that allows any platform to query a blockchain and retrieve data. Initially from third-party providers, then in-house, but the costs kept climbing as the platform scaled. Even with talented infrastructure developers on the team, there was an honest internal acknowledgment: there are people out there who can do this better than us.

“They said: we should outsource this,” Mog recalls. “But rather than outsourcing it to a third-party provider who’s basically charging what we are, if we build a subnet out of this, we incentivize people to do this better.”

How Competition Prices a Commodity

That became Blockmachine, a Bittensor subnet focused on decentralized RPC infrastructure. The mechanism it introduced was novel: miners set their own prices. So Taostats set its own internally-run miners as the baseline price to compete against. Then they would buy from the most competitive, fastest, and most reliable, according to scoring metrics.

“What we did was set up and ran the initial miners at the same cost that we had been supplying ourselves in-house. We said: we’re not going to compete, but we are going to provide the same infrastructure to ourselves. You’ve got a baseline to compete against.”

The result, he says, was immediate and striking. Miners competed the price down to a fraction of the baseline within weeks of launch.

“You can see how much money we saved as a company.”

The broader point here is about what Bittensor’s incentive structure does to a market. The top miner does not sit pretty. If they are not being challenged, they will raise their prices until competition arrives and forces them back down. The system reaches equilibrium because those most capable of delivering will price the commodity instead of a central authority setting rates.

“Rather than a centralized provider setting the pricing to a single vendor,” Mog says, “it’s the capability underneath that’s being priced.”

Blockmachine is now at the stage of onboarding a scaled marketing and business development team. The pitch to any developer currently using one of the existing RPC providers is almost comically simple: swap the URL, pay less, and if it doesn’t work, swap back.

The Thin Line Between Permissionless and Accountable

The interview had been going for some time when we arrived at the question that sits underneath every conversation about decentralized systems and institutional adoption. If one entity controls a large share of staked tokens on a supposedly decentralized network, at what point does the word “decentralized” stop meaning anything?

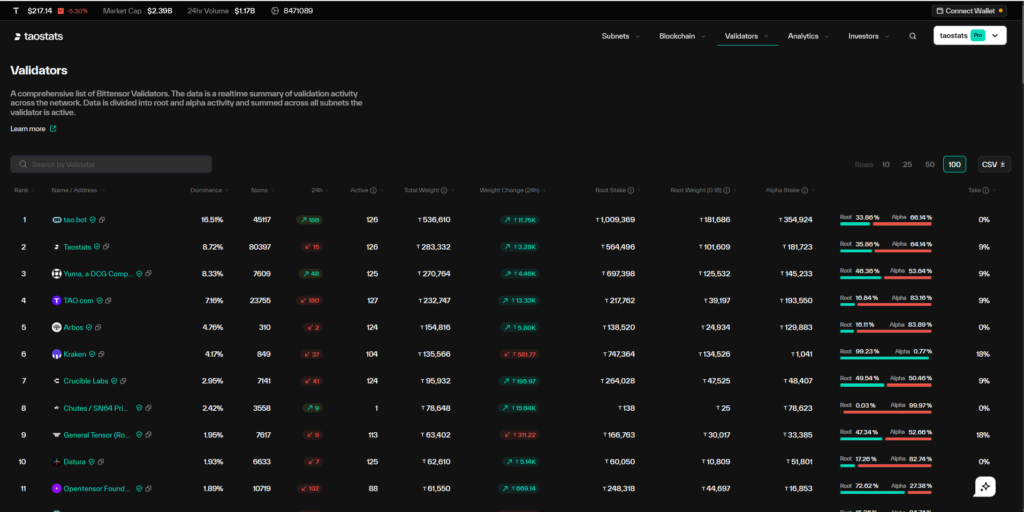

Mog gently corrected the framing. The concentration I had identified was in the top validator, Taobot, which had accumulated stake primarily because it charges a zero percent fee. Its returns are fractionally better for delegators who are not paying attention to what their stake is funding. Taostats, by comparison, takes a small percentage to fund its team and infrastructure. Taobot is not a single whale; it is the result of an information gap.

“To the uneducated, who are just looking at returns and don’t necessarily see the value of staking to someone who’s actively trying to build the value of their investment; they say, well, that’s making me half a percent more. I’ll go on them.”

But the deeper question, once corrected, was still worth asking: where is the real line between decentralized and centralized on this network? Mog’s answer was the most direct of the conversation, and he acknowledged without prompting that it places him on one side of a live debate within the ecosystem.

“I believe that permissionless protocols require a level of accountability and responsibility.”

The Case for Centralisation at the Edges

His argument is this: the base layer of Bittensor, the ability to mine, validate, create a subnet , is and should remain completely permissionless. Financial barriers exist, but there is no exclusivity gating. The cost of participation moves with demand, reaches equilibrium, and is governed by code rather than committees.

But the layer above that, the operator layer, the businesses being built on top, cannot be permissionless if they are going to sell to enterprises. Procurement requires invoices. Service level agreements require someone to call when things break. Enterprise buyers need legal accountability.

“That layer is centralized. It’s a company that has fiat payment rails, that is processing funds, that is making decisions, that is paying developers. And I think that’s the thin line that Bittensor walks on very, very well to keep one side completely decentralized and permissionless, and the other side not so much.”

On validation specifically, he acknowledged the controversy directly. The trend in Bittensor subnets is toward the owner-validator model. The person or company that created the subnet handles validation of its outputs instead of distributing that function across a decentralized set of validators. To some in the ecosystem, this feels like centralization by another name. Mog’s view is that it is specialization by necessity.

“The natural transition is that that person knows how to verify and validate their commodity better than anyone else. Having to support a distributed set group of people whose specialty is not that commodity actually harms their ability to iterate and develop and push out advancements.”

However, he notes that governance mechanisms are being developed to give distributed validators recourse if they disagree with how a subnet is being operated.

The Halving That Barely Registered

In December 2025, Bittensor underwent its first halving. Daily token emissions reduced from 7,200 TAO to 3,600, mirroring the mechanism Bitcoin uses to manage supply. In the months before it happened, there was significant anxiety in the ecosystem about what it would mean for miners and validators whose economics depended on those emissions.

I asked Mog if the halving had produced any meaningful exits from the network.

“In a word: no.”

Alphanomics: The Real Test

The reason is a piece of architecture that most outside observers missed. Eight months before the halving, in April 2025, Bittensor had launched dTAO. This new emissions model gave every individual subnet its own alpha token, with its own supply of 21 million and its own halving schedule, separate from TAO’s. Under dTAO, subnets earn in their own alpha tokens, and pay miners and validators in alpha. The TAO halving reduced TAO emissions, but it did not touch alpha emissions.

“Until there is an alpha halvening for any given subnet, there is zero effect on how much miners are being paid.”

What the halving did affect, Mog explains, was liquidity; specifically the depth of each subnet’s liquidity pool, which is fed by both alpha and TAO. Immediately after the halving, with less TAO flowing into pools, smaller amounts of capital could move prices more easily. But liquidity builds over time, particularly in popular subnets with strong emissions.

He coined a word for the economic framework subnets will need to develop before their own alpha halving arrives: alphanomics. Blockmachine is already there. It takes payment in fiat, USDC, or TAO for real services rendered, and pays miners directly from that revenue. Emissions are optional.

“If you turned off emissions, as long as we can still use the incentive mechanism to see who we owe money to and it’s on the chain — we pay those miners and it’s all there. It’s already a business that would be in no way affected by an alpha halvening.”

His view on subnets that are not there yet is unambiguous: “If they haven’t got there by their first halvening, they need to question their position within the network.”

The Plumbing Problem

The final question was the summit’s own question: what is still missing before institutional capital can flow into this space without hesitation?

Mog’s answer did not focus on technical complexity or regulatory clarity in the way many founders do. He went straight to something more mundane, and more intractable.

It’s a board-governed balance sheet that makes it as fluid to take money out as it’s put in.

The problem is not getting money into crypto. The problem is getting it back out. Anyone who has tried to move substantial profits from crypto back into the traditional banking system knows this. The rails going out are unreliable, slow, and often hostile. Institutional investors who manage fiat-denominated portfolios and answer to boards cannot participate in markets where the exit is uncertain.

“I remember sitting down with the finance minister in Dubai last year discussing this, how Dubai tried to push this forward. It’s that ability for people with very large fiat balance sheets to be able to move into crypto and then move out again. And it’s the out part.”

A Low Tolerance of Bullshit

On the question of the ecosystem’s culture, whether the unpredictability and occasional dishonesty of crypto markets is itself a deterrent, Mog is clear-eyed but not apologetic. He sees it as an honest reflection of human nature. And he believes that network-level design can progressively make the worst behaviors impossible, if not always immediately.

What he is proud of, in the network he has spent years helping to build, is something harder to quantify: a culture that is intolerant of extraction for its own sake.

“There are no meme coins. There is no extractive, pointless DeFi just for the sake of DeFi. The people governing this network have skin in the game. Not just monetary, but emotional and intellectual skin in the game. Around real use cases, not around hype. There’ll always be hype, but maybe that’s marketing. You can build a chocolate bar company and still have some hype marketing. But there’s a low tolerance of bullshit. And that’s a very nice place to be.”

There’s a low tolerance of bullshit. And that’s a very nice place to be.

We had been talking for well over an hour. As Mog stood to leave, he offered a final observation that seemed, in retrospect, to be the thesis of the entire conversation.

“I don’t do short answers.”

He doesn’t. And in a space that is often characterized by confident brevity and oversimplification, that is not a small thing.