For 250 years, the Swiss franc has done one thing better than almost any currency on earth: hold its value. While the dollar lost 80% of its purchasing power against the CHF over the last half century alone, the Swiss franc kept its head down and its reputation intact. It is the original store of value for the nervous, the cautious, and the long-term thinker. Johannes Kern wants to put it on a blockchain; and make it available to anyone in the world, no Swiss bank account required.

Kern is the Managing Director of the Frankencoin Association, the non-profit behind ZCHF, the largest Swiss franc stablecoin in existence. It’s an unusual title for an unusual project. There is no Frankencoin CEO. There is no Frankencoin headquarters in any meaningful sense. There is code, a blockchain, and an association in Zug that helps the thing grow without being in charge of it.

There’s a moment early in any good interview when you realise the person across from you is not going to play it safe. With Johannes Kern, it comes fast. Within minutes of sitting down at the Louvre Palace, he’s calling out Switzerland’s financial regulator, questioning why anyone trusts Tether, and matter-of-factly describing a future where the Swiss National Bank sits as a governance participant inside a decentralised protocol.

He came to Proof of Talk with one clear message. When we first reached out about the interview, his reaction was almost impatient: let’s talk about what it actually is. Not “a non-USD stablecoin.” Not “an alternative to dollar-denominated digital assets.” A Swiss franc stablecoin. The distinction matters to him; and by the end of the conversation, it will matter to you too.

The Dollar Is Losing. The Swiss Franc Has Been Winning For 250 Years.

The stablecoin market is a dollar monoculture. Over $300 billion in market cap, 99% of it denominated in USD. USDC, USDT are the plumbing of crypto. So why Swiss francs?

Kern doesn’t push back on dollar dominance for payments. He concedes it immediately. “If you talk about cross-border settlements, you’re really better off with just one currency. You want one currency that’s very liquid, that everyone can plug into. That’s why USDC and USDT are so strong. They’re this shared currency.”

But he draws a hard line between transacting and holding. And on holding, his case is blunt:

“The dollar lost about 80% of its value against the Swiss franc over the last 50 years. And if you go back 250 years, the Swiss franc has this historical strength as a store of value. That’s nothing new. large institutions in TradFi have always held Swiss francs because of that.”

The digital Swiss franc, in his framing, isn’t a crypto experiment. It’s just taking something that already exists in traditional finance, the CHF as a global safe-haven store of value, and making it available on-chain, to anyone in the world, without a bank.

The timing is not coincidental. The US dollar weakened significantly in 2025, and the geopolitical signal he points to is unusually concrete. The UAE leaving OPEC, he says, is “a very telling sign.” Large parts of the world are already looking for alternatives. The Swiss franc, and Frankencoin, are simply there waiting.

Who Actually Uses This Thing

When we ask who Frankencoin is actually for, Kern breaks it into three groups. And the third one is where his eyes light up.

First, domestic Swiss users who don’t want bank accounts. “We have quite a few users who don’t like banks and just live completely on-chain with Frankencoins,” he says, without any detectable irony. Switzerland has an estimated 4,000 people working in crypto who get paid in stablecoins. For them, ZCHF is a native currency.

Second, borrowers. Frankencoin offers some of the cheapest on-chain borrowing rates in the market, around 1.5% to borrow against Bitcoin. Because the Swiss franc carries historically low interest rates, the cost of minting ZCHF is structurally cheap. Compare that to a Swiss bank charging around 9% to borrow against Bitcoin, because of compliance overhead, and the efficiency case writes itself.

CrispyBull: “Frankencoin lets people hold, earn on, and spend Swiss francs without a bank account. That sounds almost too good. What’s the catch?”

Johannes Kern: “The much bigger market is the global market. It’s people with some assets who want to de-risk, who want an alternative to the dollar. This is also becoming a political question. There’s large parts of the world looking for alternatives, and the Swiss franc is just there, and on-chain is just there.”

The third group, then, is the one that makes this a multi-hundred-billion-dollar story in his telling: globally distributed capital looking for a non-dollar store of value that doesn’t require a Swiss bank account, a Swiss passport, or any relationship with Switzerland at all.

The Frankfurt Gut Punch — And Why He’s Fine With It

The most newsworthy exchange of the afternoon comes when we put a straightforward provocation to him. The first fully regulated Swiss franc stablecoin didn’t come from Switzerland. It came from Frankfurt. AllUnity, a joint venture backed by Deutsche Bank’s DWS Group, Flow Traders, and Galaxy Digital, launched a MiCA-compliant CHF stablecoin while Switzerland’s own regulator was busy tightening the screws on domestic crypto companies. Does it sting?

He’s not being theatrical. He describes a Swiss regulatory environment that has become “very hostile”, not specifically to decentralised finance, but to blockchain-based financial technology broadly. Companies in Swiss financial markets, he says, are spending their resources keeping up with constantly shifting compliance requirements rather than building anything. “It’s almost impossible to do business in Switzerland” is how he characterizes what he hears from the sector.

And then, mid-complaint, he drops something that turns the whole narrative sideways.

“We’re working quite closely with AllUnity,” Kern told us at Proof of Talk. A bridge between Frankencoin and AllUnity exists, accessible via Bitcoin Suisse, though for reasons best known to themselves, neither party has made any public noise about it.

Kern is characteristically unsentimental about why the collaboration makes sense. AllUnity, he explains, is not making money with their setup. It’s expensive to operate and their centralized, licensed structure limits what they can offer. Frankencoin, being fully decentralized, has no such constraints and can give them access to DeFi yield.

“We’re solving problems for both sides,” he says.

The Yield War Nobody Is Talking About

Frankencoin currently offers 3.5% annual yield on ZCHF. Swiss savings accounts offer materially less. Swiss banks, unsurprisingly, are lobbying against stablecoins being permitted to pay interest at all, arguing it threatens deposits.

Kern’s response is neither diplomatic nor especially worried. “The banks should just get better,” he says. He softens it slightly, but not much. His actual argument is more precise: banning yield doesn’t make yield disappear. It just moves it. Right now, he points out, stablecoin issuers who can’t pay yield directly are subsidizing kickbacks to exchanges and finding other ways to route the money. The user ends up worse off. Nothing else changes.

More importantly for Frankencoin specifically, he argues the whole debate is largely irrelevant to them. Yield restrictions are aimed at centralized issuers, entities that function like banks, taking in deposits and paying out returns. Frankencoin has no such issuer. It’s a peer-to-peer protocol.

Kern: “If you would want to prohibit that, you would have to prohibit DeFi effectively. That is a completely different can of worms, very similar to ‘let’s prohibit Bitcoin.’ Okay. You can try. What outcome does it bring you?”

The yield premium itself, he explains, comes from two structural differences versus banks. First, Frankencoin is backed by higher-volatility assets, primarily Bitcoin, which are more overcollateralized (currently around 230%) but carry a higher yield profile. Second, a decentraliszed protocol is structurally more efficient than a bank. “Banks are substantially more inefficient than a decentralized protocol by magnitudes,” he says flatly. “That’s where the difference comes from.”

Not All Stablecoins Are Created Equal

Before going further, it’s worth pausing on something the industry doesn’t always say clearly enough: Frankencoin and USDT or USDC are both called stablecoins, but the similarity largely ends there.

USDT and USDC are straightforward. For every token in circulation, the issuer holds an equivalent amount in cash, government bonds, or other fiat-equivalent assets. The peg is maintained by a centralised company with auditors, reserves, and ultimately a human being accountable for making sure one token equals one dollar. Simple, transparent in its own way, and battle-tested at scale.

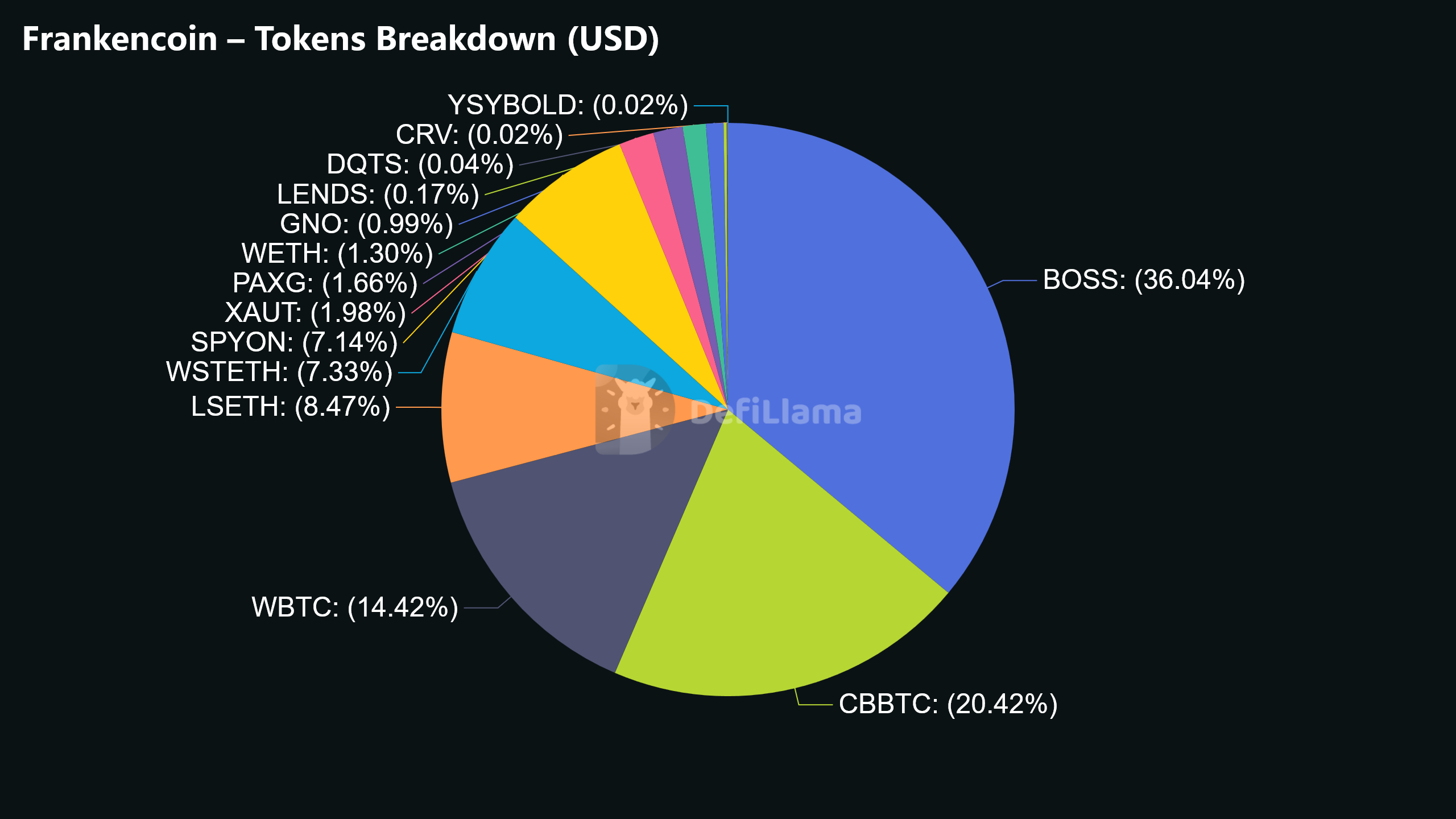

Frankencoin works differently, and more complexly. ZCHF is minted when users deposit crypto assets, primarily Bitcoin, as collateral. That collateral currently sits at around 230% of the ZCHF in circulation, meaning the system is heavily overcollateralized as a buffer against volatility. There is no central issuer, no reserve account at a bank, and no single entity standing behind the peg. Stability comes from smart contracts, auction mechanisms, and the assumption that collateral values don’t fall faster than the system can respond.

That assumption has a limit. Bitcoin dropped sharply in the days following this interview, falling to an intraday low of $59,353 on June 5, briefly breaking below the $60,000 psychological support level for the first time since early 2026, and down over 45% from its October 2025 all-time high. Frankencoin’s TVL tells the story directly: it fell 43.8% in a single week, from $68.49M to $38.51M, as borrowers closed positions to avoid being liquidated. The protocol held its peg and TVL has since recovered to $63.32M. But the stress test was real. When crypto collateral loses value rapidly, the overcollateralization buffer shrinks. If it shrinks far enough, fast enough, the risk of a depeg becomes existential. This is not a flaw unique to Frankencoin. It is the inherent tradeoff of any decentralized, crypto-backed stablecoin.

Kern would argue — and does, in this interview — that the transparency of the on-chain system is precisely what makes it more trustworthy, not less. Every collateral position is visible in real time. There are no hidden risks, no opaque reserve reports. But visible risk is still risk, and readers should understand what they’re looking at before they decide whether 3.5% yield is worth it.

“Why Should You Trust Something Nobody Is In Charge Of?”

It’s the question that stops most people from ever engaging with decentralized finance. Tether has a CEO. Circle has auditors and GENIUS Act compliance. Frankencoin has code. For someone who’s never touched crypto, why would they trust it?

Kern’s first answer is a single word.

“Code.”

Then: “Turn the question around. Tether — for a very long time and still is — it’s not a very transparent company. So why do you trust them? Do you know Paolo? Is he a good guy?”

He’s not being glib. His point is that trust in centralized institutions is itself a kind of blind faith, one we’ve normalized through familiarity. With Frankencoin, “every block you can audit on-chain. There is no one who could take any decision, who could do something which you do not know about in advance. Everything is verifiable, everything is transparent.”

We push back. We grew up trusting banks. That’s just how we know finance.

“Exactly,” he says. “Core banking systems are a lot more fragile than blockchain, massively more fragile. And a lot more complex. Blockchain is reducing that complexity. It makes it actually verifiable. A person can go there and say: this is what is there. I can be sure this is actually there. It’s not just stale data from somewhere.”

The Dream: 100 Billion Francs, the SNB, and a Meta-Stablecoin

We close the conversation with the biggest question. If this works, if the digital Swiss franc becomes real financial infrastructure, what does it actually look like in ten years?

Kern is clear on what it isn’t. He doesn’t see Frankencoin as a domestic payment network. Centralized stablecoins, he says, are more efficient for that. Where he sees the real opportunity is in what he calls the “meta-stablecoin”: a decentralized, composable layer that anyone building on the Swiss franc plugs into.

He reaches for an analogy. “I like the term ‘Lego of moneys.’ You have Legos, you can combine them together frictionlessly. No written contracts with anyone. No silos, no islands. Just working together.”

In this vision, AllUnity might issue a regulated CHF stablecoin for institutions. UBS might issue one for private banking clients. A neobank might wrap it for retail. But underneath all of them, the shared fabric, the on-chain reserve layer, is Frankencoin.

And then he says the quiet part loud.

“If you paint the dream picture — 50 years down the line — 100 billion assets or more, the Swiss National Bank being one of the players actively shaping the development of Frankencoin, a governance token holder. It’s this meta-stablecoin that everyone who needs a Swiss franc on-chain just plugs into.”

The Swiss National Bank. A governance participant in a decentralized protocol built by a non-profit in Zug.

It’s an audacious vision. It’s also, in the logic of the conversation that preceded it, not entirely unreasonable. The Bank of England is already thinking about digital currencies that aren’t dollar-denominated. Kern is on a panel with them the following day. Switzerland, meanwhile, watches from the sidelines while a German consortium launches the first regulated Swiss franc stablecoin.

“I hope it stings them really hard,” he said at the beginning. By the end, it’s clear he’d rather they just showed up.